Bedford Township Financial and Tax Information Page

Bedford Yes Home

Bedford Township Home

The purpose of this page is to keep Bedford Township residents informed concerning the revenue and expenditures for Bedford Township government. Information concerning property tax and other taxes are also listed on this page.

Quick Links: Current Salary Info Property & Land Search

Bedford Township Financial Information:

Click here to view a copy of the 2014-15 budget that was approved at the June 3, 2014 Bedford Township Board Meeting.

Click here to view current financial statements that are posted on the Bedford Township web site.

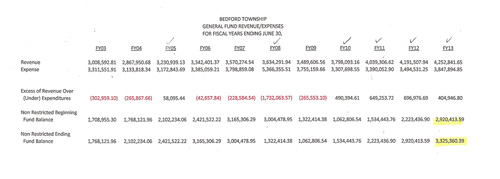

General Fund Comparison for 2003-2013

Click here to view a copy of the Bedford Township General Fund Revenue/Expenses for Fiscal Years 2003 to 2013 ending June 30.

The ending balance for each year is also listed, which is the amount of excess money in the account (sometimes referred to as the "Rainy Day Fund"). For example on June 30, 2013 the General Fund has a balance of over $3.3 Million Dollars in the "Rainy Day Fund". This balance is "Non Restricted", which means that the Bedford Township Board can approve to spend some or all of the excess funds as they wish. For example in 2007-2008 the Bedford Township Board approved to spend $1 Million Dollars toward the construction of the new Bedford Township Hall. See the newspaper articles listed below for the details of the expenditure for the new Bedford Township Hall.

Click here to view the adjusted Balance Sheet for June 30, 2014 which shows a General Fund Balance of $3,888,363.63 (This page was part of the board packet for the Bedford Township Board Meeting on August 12, 2014.)

Newspaper articles concerning the construction of the new Bedford Township Hall in 2007 ($1 Million Dollars approved from the General Fund toward the construction cost):

Toledo Blade September 20, 2006 "Toledo Builder wins contract for a Municipal Hall"

Toledo Blade September 12, 2007 "Bedford Township's $2.9 Million Government Center To Open Soon"

Current Salary Information for Bedford Township Officials & Employees

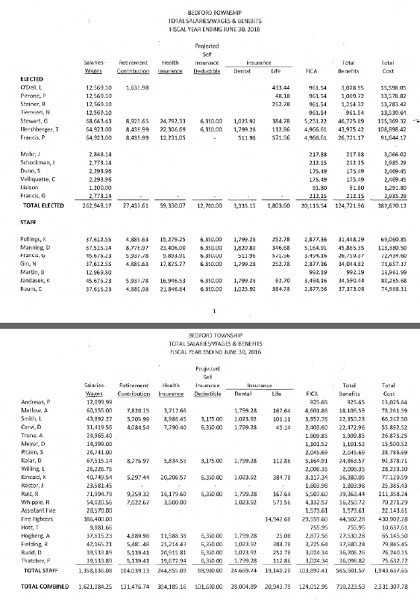

For Fiscal Year Ending June 30, 2016

Click here to view the current salaries and fringe benefits for Bedford Township elected officials and Bedford Township employees for the Fiscal Year Ending June 30, 2016. The source for the information: 2015-16 General Fund Budget & General Fund for Fiscal Year Ending June 30, 2016. The salary & benefits information is contained on 3 pages.

Fiscal Year Ending June 30, 2014

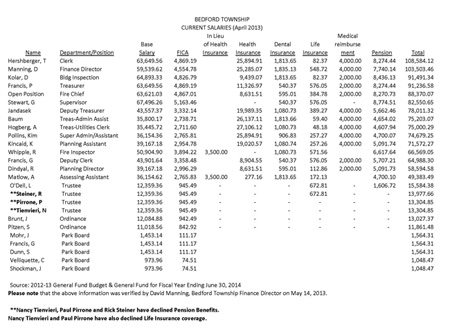

Click here to view the current salaries and fringe benefits for Bedford Township elected officials and Bedford Township employees. The source for the information: 2012-13 General Fund Budget & General Fund for Fiscal Year Ending June 30, 2014. Please also note that I sent a copy of the information to David Manning, Bedford Township Finance Director by e-mail. He verified on May 14, 2013 that the salaries and fringe benefits that I have listed are correct.

Click here to view the current salaries and fringe benefits for Bedford Township elected officials and Bedford Township employees. The source for the information: 2012-13 General Fund Budget & General Fund for Fiscal Year Ending June 30, 2014. Please also note that I sent a copy of the information to David Manning, Bedford Township Finance Director by e-mail. He verified on May 14, 2013 that the salaries and fringe benefits that I have listed are correct.

At the Bedford Township Board Meeting on April 16, 2013 there was extensive discussion concerning the Compensation Committee’s Recommendation to give raises to the elected officials of Bedford Township. (Click here to view the video of the discussion, go to the 47 minute mark for the discussion and the 1 hour 49 minute mark for the vote on this item.) At the meeting former Bedford Township Supervisor LaMar Frederick spoke during public commentary time concerning the issue of the recommendations. He stated in his comments that Bedford Township elected officials are paid more presently than elected officials at the county level. (Click here to view his comments, go to the 1 hour and 25 minute mark of the video.)

a. Click here to view the Compensation Committee's recommendation (Go to page 37 & 38 of the board agenda).

b. Click here to view information concerning how Bedford Township salaries compare to other townships in Monroe County. This information was obtained from the Bedford Township Compensation Committee Chairman. Also included is a copy of the minutes of the Compensation Committee meeting of March 18, 2013.

c. Click here to view a comparison of Bedford Township salaries with additional Monroe County Townships not listed in "b" above.

d. Click here to view information concerning how Bedford Township salaries compare to other townships in the State of Michigan based on similar population to Bedford Township. Also listed is the current Cost-of-Living Adjustments published by the Social Security Administration. This information was obtained from the Bedford Township Compensation Committee Chairman. Also included is a copy of the minutes of the Compensation Committee meeting of March 18, 2013.

Click here to view a copy of the 2010-2011 proposed budget for Bedford Township. The statement will show what was budgeted for 2008-2009, 2009-2010 and what is proposed for 2010-2011 for all Township General Fund accounts and all special fund accounts. The 2010-2011 budgeted amounts appear in the far right column of each page. The financial year Bedford Township starts on July 1, 2010 and ends on June 30, 2011.

Click here to read a copy of the Revenue & Expenditure Report for Bedford Township for the month ended January 31, 2010. Since Bedford Township is on a fiscal year from July 1 to June 30, this should give residents a good idea of what was budgeted for 2010 and what has been spent so far this year. Information provided by the Bedford Township Clerk's Office.

Click here to read a copy of the Revenue & Expenditure Report for Bedford Township for the month ended June 30, 2009. Since Bedford Township is on a fiscal year from July 1 to June 30, this should give residents a good idea of what was budgeted and spent for the year of 2008-09. Information provided by the Bedford Township Clerk's Office.

Click here to read a copy of the Revenue & Expenditure Report for Bedford Township for the month ended April 30, 2009. This report also will show budget amounts for each area and will show year-to-date totals thru April 30, 2009. This information was provided by the Bedford Township Clerk's Office. As we receive new reports, we will post them on the web site.

Click here to view articles concerning "Where Do My Tax Dollars Go?" that were published in the Bedford Township Update Spring 2011.

Sample Property Tax Statements:

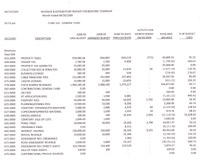

Summer Tax Statement 2019:

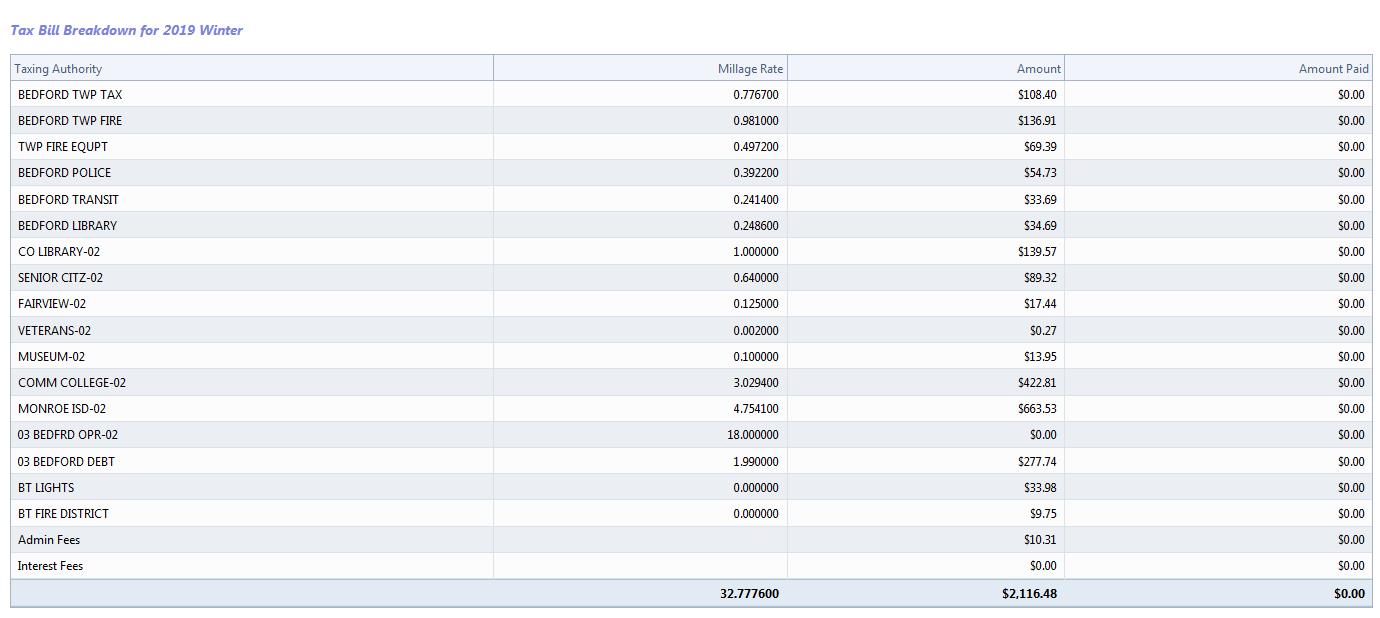

Winter Tax Statement 2019:

Steps to find your property tax statement or any property owner in Bedford Township:

1. Go to the Bedford Township web site: http://www.bedfordmi.org/

2. Scroll down the home page and click on the right hand side of the page "Property and Tax Info"

3. On the next page type in your last name or the last name of the person's property that you want to search. After you enter the last name, click on the "Search" box at the far right.

4. Click on the person's name that is listed in the name section.

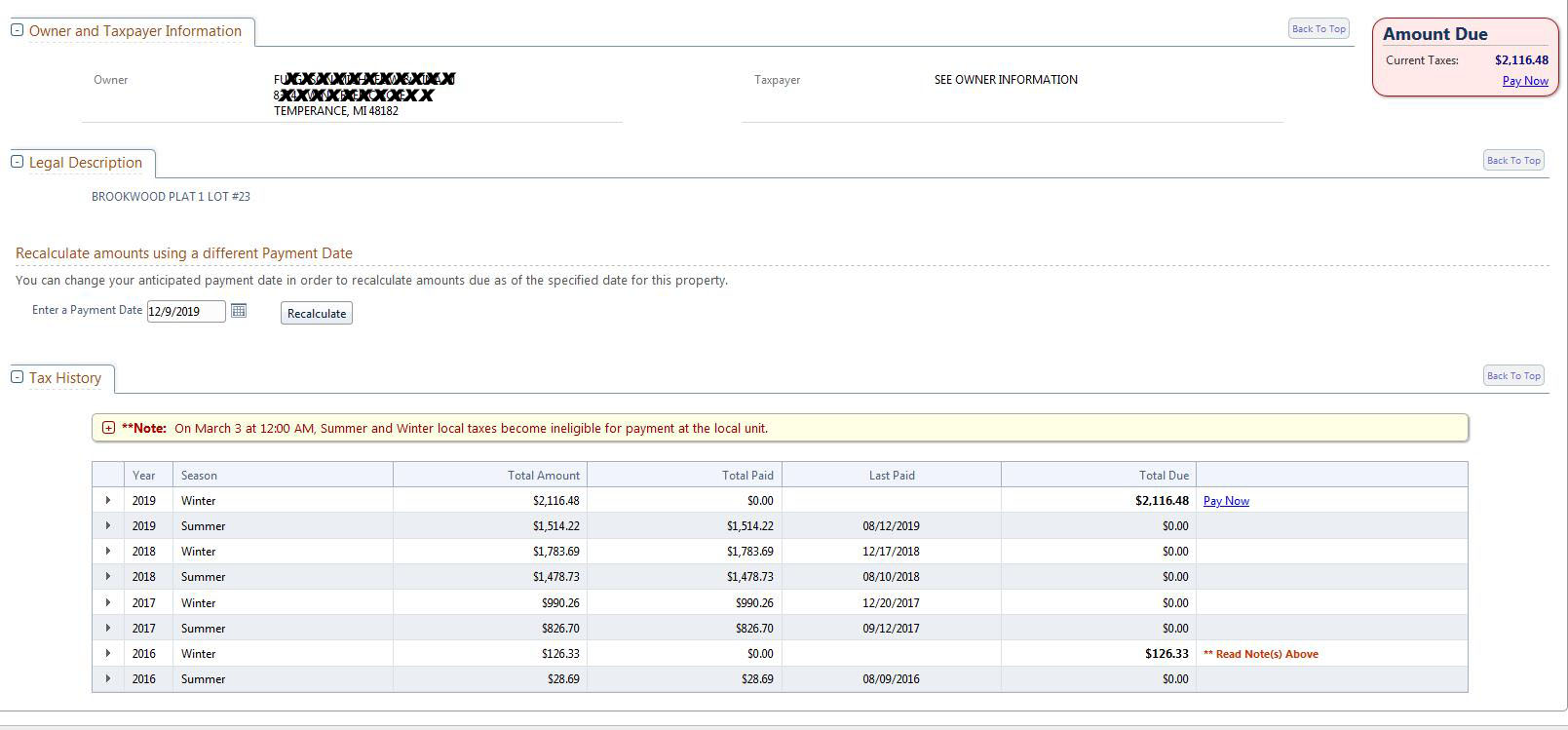

5. This will bring up the property tax page:

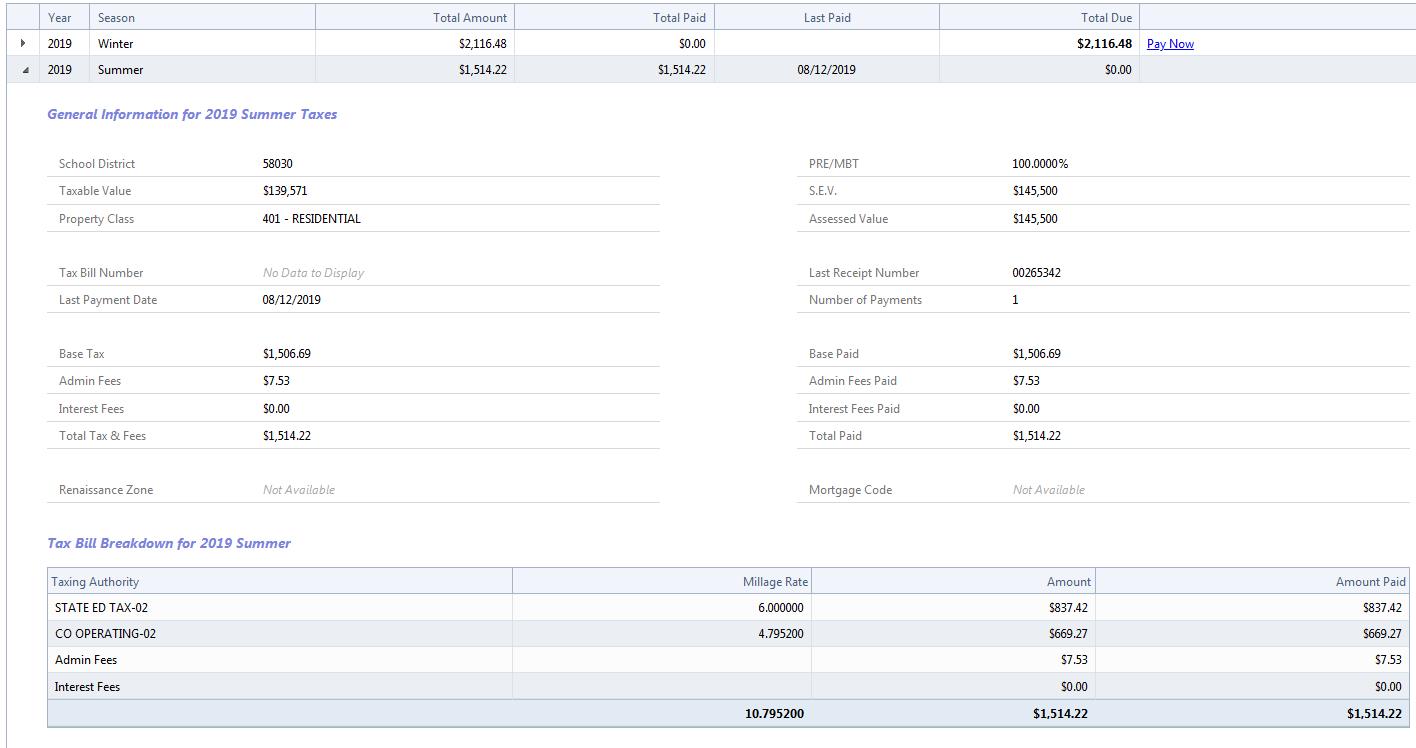

6. To view the complete Winter or Summer tax bill click on the the "little arrow" at the left of the year and it will bring up the following tax bills for 2019 as examples:

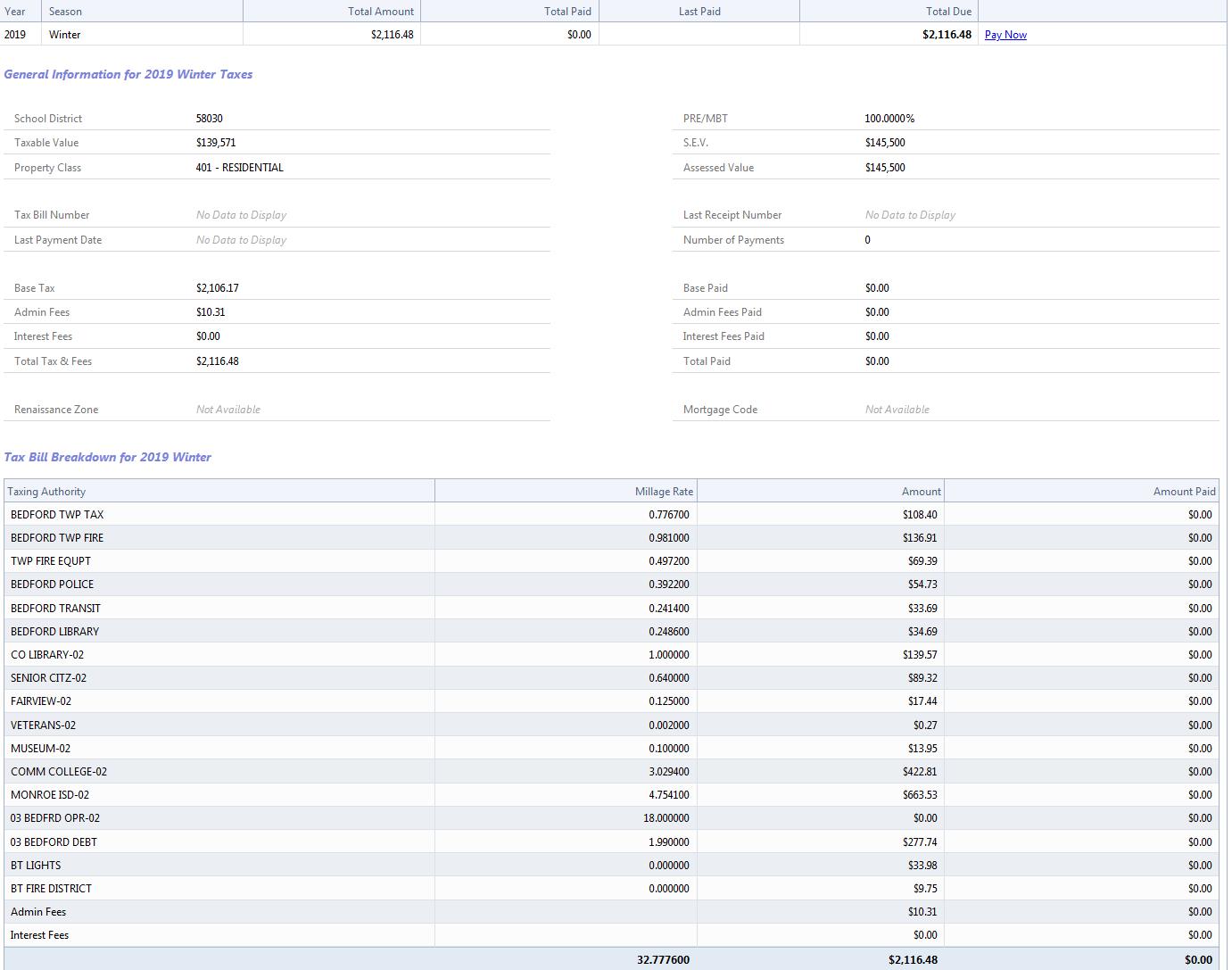

The graphic at the left are the current tax millages that Bedford Township Residents pay each year.

Listed below is an explanation of each tax:

BEDFORD TOWNSHP 2015 SUMMER TAX BILL

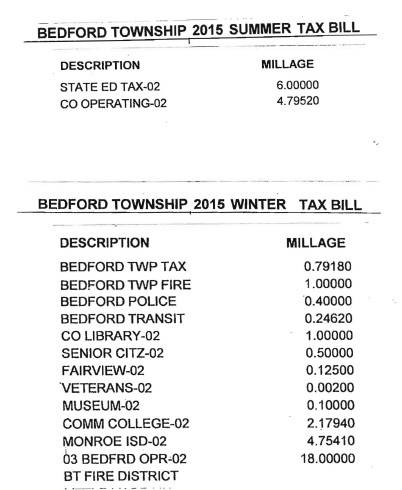

STATE ED TAX-02 (Bedford Public Schools Operating) MILLAGE 6.00000:

In 1994, the voters of the state of Michigan approved ballot Proposal A by a margin of 1,681,541 to 750,952 in a special election held on March 15, 1994. This proposal (Senate Joint Resolution S), in part, imposed an additional 2% rate on the sales and use taxes and capped the rate of annual increases in taxable value to the rate of inflation or 5%, whichever is less. When the property is transferred, it is assessed in the following year at one half of true cash value. In addition, 1993 PA 331 created the State Education Tax Act, imposing a six-mill state education tax. 1993 PA 331 created the State Education Tax Act, imposing a six-mill state education tax levy on all property subject to the general property tax. Public Act 312 of 1993 allows local school districts to levy not more than 18 mills for school operating purposes or the number of mills levied in 1993 for school operating purposes, whichever is less. Principal residences and, pursuant to 1994 PA 136, qualified agricultural property are exempt from the 18-mill levy. A homeowner’s principal residence is defined, in part, to mean that portion of a dwelling or unit in a multiple dwelling owned and occupied as the owner’s principal residence. A homestead also includes all of an owner’s unoccupied residential property adjoining or contiguous to the dwelling owned and used as the owner’s principal residence, any portion of a principal residence rented or leased as a residence to another as long as that portion rented or leased is less than 50% of the dwelling’s total square footage of living space, a life care facility, or property owned by a cooperative housing corporation and occupied as a principal residence by tenant stockholders. This is not a voted millage, so the millage does not expire.

View “Michigan Taxpayers Guide 2014” for additional information concerning taxes in Michigan.

Click here to view Basics of Michigan School Funding July 2015

CO OPERATING -02 (Monroe County Operating) MILLAGE 4.79520:

Michigan’s counties derive their authority from Article VII of the Michigan Constitution and Chapters 45 and 46 of the Michigan Compiled Laws, which classifies counties as bodies politic and corporate in the State of Michigan. The constitution vests all legislative and executive power in a board of commissioners with membership based on the number of townships and cities in the county. Membership of the boards ranges from five to twenty-six members. The constitution insists that all statute and constitutional powers of counties be construed in their favor when exercising enumerated powers; however, the county may not take action which is not specifically permitted by state law or by the constitution. Thus, Michigan is a Dillon’s Rule state.

County Finance:

County commissions have budgetary authority in Michigan. Counties may levy property taxes to fund county operations. Counties may levy taxes in conjunction with other political subdivisions; however, the aggregate tax levied by all combined must not exceed eighteen mills, unless the county electors choose to increase that limit. Electors may increase the limit up to fifty mills on the dollar for a period no longer than twenty years. Counties also receive fifteen percent of all sales tax revenues collected within the state, to be apportioned based on population. Per constitutional limitation, no county may go into debt to exceed ten percent of the assessed valuation of the property within the county’s corporate limits. The current Monroe County Millage is 4.7950 and does not expire. (Perpetuity)

View “Monroe County 2014-15 Proposed Budget” for complete information concerning the Monroe County Budget

Click here to view the Monroe County Tax Rate request form which explains the tax rates for county taxes.

BEDFORD TOWNSHP 2015 WINTER TAX BILL

BEDFORD TOWNSHIP TAX MILLAGE 0.79180

The Michigan Constitution and state statutes limit the amount of property tax millage that townships can levy for general township operations. General Law townships (such as Bedford Township) are allocated at least 1 mill from the constitutionally limited 15/18 mills allocated among townships, the county, public schools and the intermediate school district. Charter townships, like cities, do not share in this allocated millage, but townships chartered by a referendum may levy up to 5 mills. Townships chartered by board resolution after Nov. 22, 1978, must have a vote of the electors authorizing the levy of up to 5 mills. In either case, the 5-mill limit may be increased up to 10 mills with a vote of the electors .Townships also utilize other sources of revenue to support services. User fees, permits, fines and special assessments on real property are the most frequently used sources. This is an allocated millage, therefore taxpayers do not vote on this millage. Currently the Bedford Township Millage rate is 0.79180.

View the following for additional information concerning how the millage is allocated and the budget for Bedford Township:

Current Financial Statement and Budget for Bedford Township

2016 Tax Rate Request for Bedford Township

Michigan Township Association (MTA)

BEDFORD TOWNSHIP FIRE MILLAGE 1.000

A Bedford Township Fire Levy Replacement measure was on the August 7, 2012 ballot. This measure was approved

YES 3,748 (67.67%)Approved NO 1,791 (32.33%)

This measure sought to replace the current city fire levy with one set at a rate of $1 per $1,000 of assessed value for a period of four years in order to continue pay for the fire department operational costs in the township.

The question on the ballot:

Shall the annual tax rate limitation imposed under Article IX, Section 6 of the Michigan Constitution of 1 mill ($1.00 per $1,000.00 of taxable value) be increased, and shall the Township of Bedford be authorized to levy 1.0 mills ($1.00 per $1,000.00 of taxable value), upon the taxable real and tangible personal property within the Township of Bedford, Monroe County, Michigan for a period of four (4) years from 2013 through 2016 inclusive, for the purpose of providing funds to the Bedford Township Fire Department to be used for general operations and capital expenditures, and for maintenance on Fire Department buildings, equipment and building sites? The estimated revenue for the first year of the levy, if the proposition is approved, shall be approximately $960,000.00. This new 1.0 mill levy is not a renewal but it replaces an expired 1.0 mill fire protection millage, which has been reduced over the last few years to .8980 mills by the required Headlee millage rollbacks. (This millage expires in 2016)

Click here to view additional information

2016 Tax Rate Request for Bedford Township

BEDFORD POLICE MILLAGE 0.40000

In August of 2012 Bedford voters approved a 0.4-mill, seven-year renewal of a measure that pays for the four deputies under a contract with Monroe County Sheriff’s Office. The millage was expected to generate $388,000 its first year. A taxpayer with a $100,000 home would pay $20 a year. (This millage expires in 2019)

Click here to view additional information

2016 Tax Rate Request for Bedford Township

BEDFORD TRANSIT MILLAGE 0.24620

A Bedford Township Transit Levy Renewal measure was on the August 7, 2012 ballot. This measure was approved;

YES 2,950 (54%)Approved NO 2,513 (46%)

This measure sought to renew the current city transit levy which is set at a rate of $.24 per $1,000 of assessed value for a further three years in order to continue to pay for the Lake Erie Transportation services and bus services offered in the township.

The question on the ballot:

Shall the expired previously voted increases in the tax rate limitation imposed under Article IX, Section 6 of the Michigan Constitution of .20 mills ($.20 per $1,000 of taxable value) and of .05 mills ($.05 per $1000.00 of taxable value), which combined, totals .25 mills ($.25 per $1,000.00 of the taxable value), and which is reduced to .2464 mills by the required Headlee millage rollbacks, be renewed at .2462 mills ($.2464 per $1,000.00 of the taxable value), upon the taxable real and tangible personal property within the Township of Bedford, Monroe County, Michigan, for a period of three (3) years from 2013 through 2015 inclusive, for the purpose of providing funds to the Lake Erie Transportation Commission for Bedford Dial-A-Ride bus service in Bedford Township? The estimated revenue increase for the first year of the levy, if the proposition is approved, shall be approximately $239,188.54. (This millage expires in 2015) A new millage request was approved by the Bedford Township Board for the March 8, 2016 Presidential Primary election.

Click here to view Lake Erie Transit web site.

Click here to view a newspaper article in the Bedford Now concerning the millage request that was approved by the Bedford Township Board for the March 8, 2016 Presidential Primary election.

2016 Tax Rate Request for Bedford Township

COUNTY LIBRARY-02 MILLAGE 1.000

On August 7, 2012 voters renewed the 1-mill tax that provides about 83 percent of the funding for the library’s 16 branches and programs around the county. The vote was 16,913 to 7,507. The tax will be levied for the next eight years. For the owner of a $150,000 home, the tax will be about $75 a year. (This millage expires 2020).

Click here to view a newspaper article in the Monroe News concerning the millage vote on August 7, 2012.

Please note that Bedford Township voters passed a millage in 2002 to renovate the Bedford Branch Library. This millage ended in 2012. Included in that millage was money allocated for local operation until 2012. The Township has asked for additional millage for library operation in the past. The question has also been asked why would there be a local millage when we already pay a County Library millage. The County millage is used for things such as employees, books, and other materials associated with the distribution of library materials. Each local branch’s taxpayers must maintain their own facility when they choose to have a local branch within their township. Bedford Township taxpayers must maintain the building/facility and operation of the facility. Items such as utilities, maintenance, improvements, furnishings, grounds, etc. are paid for by the taxpayers of the local branch, whether that money comes from the General Fund or extra voted millage. The taxes collected from a local millage then would be used to pay for the operation of the facility, but not the employees or books. At the December 1, 2015 Bedford Township Board Meeting the board approved putting a millage request on the March March 8, 2016 Presidential Primary election. They retracted the request at their December 15, 2015 Board meeting at the request of the Bedford Township Library Advisory Committee as they have approximately $500,000 in their local Township account for local operation which should take them through 2016. After 2016 the Bedford Township Board would be responsible to pay for local operation from the Township's General Fund.

Please also note that in Bedford Township no additional township millage proposals can be placed on any ballot without the Township Board determining the ballot wording and voting at a public meeting to place it on the ballot of a particular upcoming election. If there is additional school millage requested by the school district that ballot wording and dollar amount would be approved by the School Board. School millage is not governed by the Township Board. Since it is the voters in Bedford Township who determine if they want to pay extra tax dollars for specific services, then I believe the Township Board should give the public the ability to make that decision through the ballot proposal process. It is then determined by a majority vote of the electors if the additional tax dollars should be collected or not.

Click here to view the newspaper article in the Monroe News concerning a millage request in 2014 for additional funds for library operation, which was defeated by Bedford Township voters.

Click here to view the newspaper article that appeared in the Toledo Blade concerning the 2014 millage request.

SENIOR CITIZENS -02 MILLAGE 0.50000

On August 7, 2012 a countywide millage to fund a range of senior services was renewed by voters. The tax passed overwhelmingly 19,243 to 5,577 votes. Nearly $3 million the millage raises locally usually is matched by a like amount in state and federal funding. The renewal enables the county to levy up to a half-mill for four years. The money funds more than 26 agencies and programs that supply services to senior citizens around the county. (This millage expires in 2016)

Click here to view the Monroe County Commission on Aging web site.

Click here to view the newspaper article in the Monroe News concerning the millage results for August 7, 2014.

FAIRVIEW-02 MILLAGE 0.12500

The purpose of this millage is to provide funding for the Monroe County Fairview program which provides care and transitional shelter to people that are disabled and homeless. Without Fairview's program Monroe County will have these individuals/future individuals living on the streets. The total operating budget of the Fairview Home infirmary for 2013 is $1,432,897 with $383,099 in fund balance carry forward expenditures. The Fairview Home is funded by $1,087,912 in property tax revenue and $330,000 from other operationally generated revenues. (This millage expires in 2020)

Click here to view Fairview revenue & expenditures for 2011-2014

Click here to view the 2014-15 Monroe County Line Item Budget for information on Fairview (See Page 7 (R-6)

VETERANS-02 MILLAGE 0.00200

On November 24, 2009, the Monroe County Board of Commissioners approved a Resolution Approving an Indigent Veteran’s Millage of up to 1/10th of a Mill to be levied annually to fund indigent Veteran’s expenses as Public Welfare programs. Additionally, the Board of Commissioners approved a Resolution to reorganize the Monroe County Soldier’s Relief Commission to the County Department of Veteran’s Affairs and to dissolve the Soldiers’ Relief Commission in accordance with Public Act 192. The total operating budget of these programs for 2013 is $264,653 with $180,495 in fund balance carry forward expenditures. ( This is an allocated millage, therefore taxpayers do not vote on this millage.)

Click here to view the 2014-15 Monroe County Line Item Budget for information on the Veterans Millage (See Page 7 (R-6)

MUSEUM-02 MILLAGE 0.10000

On August 7, 2012 voters approved a millage to fund the operations of the Monroe County Museum and its programs. The millage is for a levy of up to .10 mills per $1,000 of taxable valuation. The millage is for a period of ten (10) years, from 2012 through 2021. The estimated annual revenue from the millage is $543,956. No General Fund appropriation is included in the Historical Commission budget in 2013. All revenue collected from the millage for this purpose will be deposited into a restricted fund to pay all costs to staff and operate the Historical Commission programs, expenses and services. The Board of Commissioners shall appropriate all funds from the millage revenue within this restricted fund. (This millage expires in 2021)

Click here to view the 2014-15 Monroe County Line Item Budget for information on concerning the Museum Millage (See Page 7 (R-6)

COMMUNITY COLLEGE-02 MILLAGE 2.17940

For Monroe County Community College, the taxation district is Monroe County. As such, all millage elections for the College must be approved by the county electorate. In 1964, county voters approved a 1.25 mil levy to create the College. In 1980, a 1 mill increase was approved. The rate remained at 2.25 mils until 1994 when revised tax legislation (the Headlee Amendment) introduced a rollback provision. Such rollbacks are calculated annually and are required when the increase in “adjusted” property tax values exceeds the rate of inflation. The current millage rate for the College is 2.1794, and the 2.25 millage rate can only be reinstated by a vote of the people. (This millage does not expire. (Perpetuity)

Click here to view the “Monroe County Community College General Fund Revenue 2013”

MONROE COUNTY ISD MILLAGE 4.75410

The ISD budget will require a levy of 1.2763 mills for the General Fund and 3.4778 mills for the Special Education Fund. For a total of 4.75410 mills. The Monroe County Intermediate School District (MCISD) is the regional educational agency for this portion of the State of Michigan. The MCISD is comprised of nine constituent public school districts, two charter schools, and 15 non-public schools. (.19866 expires in 2017; The rest does not expire. (Perpetuity)

Serving as a link between local districts and the Michigan Department of Education, the MCISD connects Monroe County youth -- from birth through age 26 -- with specialized education services and resources in schools and community settings throughout the area. In addition to special education services provided in students' home districts, the MCISD operates the Monroe County Educational Center for children with complex developmental disabilities, the Monroe County Transition Center for secondary students with disabilities who polish their personal living and employability skills in real-life settings, and Holiday Camp, which is a summer program that offers enrichment and respite activities for students. The MCISD also provides academic programming for students in the juvenile justice system at the Monroe County Youth Center.

Additionally, the MCISD collaborates with a wide range of community agencies and service organizations to develop strategies that address school safety, early childhood development and nurturing, substance abuse prevention, and other social issues that affect students, their families and our community at large. The MCISD offers professional development opportunities to educators throughout the year, providing presenters and forums in which teachers, administrators and classroom personnel can explore the best practices and emerging strategies that take learning to the next level of excellence.

Click here to view additional information concerning the Monroe County ISD

Click here to view MCISD 2015-16 Budget

03 BEDFORD OPR-02 MILLAGE 18.000

In 1994, the voters of the state of Michigan approved ballot Proposal A by a margin of 1,681,541 to 750,952 in a special election held on March 15, 1994. This proposal (Senate Joint Resolution S), in part, imposed an additional 2% rate on the sales and use taxes and capped the rate of annual increases in taxable value to the rate of inflation or 5%, whichever is less. When the property is transferred, it is assessed in the following year at one half of true cash value. In addition, 1993 PA 331 created the State Education Tax Act, imposing a six-mill state education tax. 1993 PA 331 created the State Education Tax Act, imposing a six-mill state education tax levy on all property subject to the general property tax. Public Act 312 of 1993 allows local school districts to levy not more than 18 mills for school operating purposes or the number of mills levied in 1993 for school operating purposes, whichever is less.

Most property owners are exempt from paying this millage because they receive a PRINCIPAL RESIDENCE EXEMPTION. View “Michigan Taxpayers Guide 2014” for additional information concerning the exemption and how taxes are calculated.

A principal residence is exempt from taxes levied by a local school district for operating purposes of up to 18 mills. A homeowner’s principal residence is defined as “the one place where an owner of the property has his or her true, fixed, and permanent home to which, whenever absent, he or she intends to return and that shall continue as a principal residence until another principal residence is established.” Property owners may claim only one exemption. A husband and wife, filing income tax returns jointly, are generally entitled to no more than one principal residence exemption, although the law allows a temporary, additional exemption for up to 3 years on an unsold homestead, and allows members of the armed forces to retain their exemption if they rent their home while away on active duty. To be eligible for the homeowner’s principal residence property exemption in 2014, a taxpayer must have claimed an exemption by filing an affidavit with the local tax collecting unit on or before June 1, 2014 for the immediately succeeding summer tax levy and November 1, 2014 for the immediately succeeding winter tax levy. Exemptions filed in prior years are valid until rescinded.

Click here to view Basics of Michigan School Funding July 2015

Additional Resources Concerning Taxes in Michigan

Outline of the Michigan Tax System by the Citizens Council of Michigan

Basics of Michigan School Funding July 2015

(The information below was taken from the Bedford Township web site.)

How is property assessed?

Real property assessments are based on market values and are assessed yearly by the assessor's department. Assessment notices are mailed to taxpayers of record in January or each year. An important part of assessing property is the appeal process. Real property assessments can be appealed at the March board of review.

Personal property assessments originate from a filing of a statement by the taxpayer. If a personal property statement is not furnished the assessor, he/she is authorized to assess such amount of personal property as deemed reasonable and just. The business owner is required by law to report the value of property owned on a personal property statement form provided by the local assessor. Assessment notices are also mailed to business personal property owners in January of each year. Personal property assessments can also be appealed at the March board of review.

FOR MORE INFORMATION ON PROPERTY ASSESSMENTS CONTACT THE TOWNSHIP ASSESSOR'S DEPARTMENT AT (734) 847-6791 (734) 847-6791.

How is my tax rate determined?

The summer tax rate is the State Education Tax determined by the State of Michigan, which is 6 mills. The Monroe County Operating Tax - 4.7952 mils.

The winter tax rates are Township, Township Police, County Library, County Seniors, Special Education, Community College, School Operating and School Debt set by each taxing entity during the month of September.

What is the difference between assessed value and taxable value?

Taxable value (TV) is the value used to compute your tax bill and applies to real property only. "TV" is determined yearly as the LESSER of assessed value (market based as determined by assessor) and capped value. Capped value is the prior year's taxable value, less taxable value of losses, "capped" by an increase of the lesser of 5% or the rate of inflation, plus assessed value of additions. Taxable value becomes uncapped when property is sold or transferred.

What is a Principal Residence Exemption and how do I know if I have one?

A Principal Residence Exemption entitles the owner of real property an exemption from the 18* mills of school operating tax for the percentage of taxable value used as a primary residence. The Principal Residence Exemption must be claimed on a form approved by the Michigan Department of Treasury. The Principal Residence Exemption for your property will be included on your assessment notice expressed as a percentage. The Principal Residence Exemption percentage will also be displayed on your summer and winter tax bill. A Principal Residence Exemption of 100% means your property is exempted from 100% of school operating taxes. Voted school bonded debt millages are NOT exempted.

* Or less subject to Headlee Amendment roll back

FOR QUESTIONS ON YOUR PRINCIPAL RESIDENCE EXEMPTION PLEASE CONTACT THE TOWNSHIP ASSESSOR'S DEPARTMENT AT (734) 847-6791 (734) 847-6791.

Property & Land Search Information :

Property & Land Search Information for Bedford Township

The Bedford Township web site has a page called “Property/Tax Info” which can be very useful if you would like information concerning any parcel in Bedford Township. Information that is available is:

Here are the directions on how to access the information:

By Address: For this example, let’s say you are interested in a piece of property located on Erie Road and have a general idea of the address but do not know the exact address and you know what the house looks like. Under the “Address Search Fields” type in “Erie”, in the “street number” box type “10” in the first box and “500” in the next box (this will be the range of the addresses), next go to the bottom of the page to where is says “records per page” and click on the circle next to “50” and then click on the “search” box at the bottom. The next page that opens will give you all of the parcels in the range that you specified. It will give you the parcel number, the owners name and property address. If you want to see the information on a particular parcel, just click on the “parcel number” which should be highlighted in blue. You can view a photo of the home and other buildings that are on the property by clicking on the “Images/Sketches” tab that is located on the left hand side of the page.

By Parcel Number Search: Just type in the parcel number next to the “parcel number box under “Parcel Number Search Field”, then go to the bottom of the page and click on the “search” box.

By Owners Name: Just type in the last name of the owner in the “owners name” box under the “Owner Search Field”, then go to the bottom of the page and click on the “search” box. The next page will give you the list of all parcels owned by residents with that last name.

Please note that there is a “help” button on the upper right-hand corner of each page if you need more information on a specific item.

Related Newspaper Articles:

Bedford Now April 9, 2011: Letter to the editor by Frank Knoll "Problems need better solution than just money"

Toledo Blade March 29, 2011: "Rage over roads fills Bedford Township forum"

Monroe Evening News March 28, 2011: "The fight is on to fund road improvements"

Toledo Blade March 23, 2011: "Dundee grows as Michigan declines" Complete population changes for local, county and the state of Michigan are posted.

Toledo Blade Neighbors March 23, 2011: "Lot, burial costs to rise in Bedford Township."

Monroe Evening News March 16, 2011: Letter to Editor by Jim Goebel "Businesses gain;seniors and schools lose under Snyder's plan"

Toledo Blade June 9, 2010: "Bedford Township Budget Lacks Big Cuts, Layoffs"

Monroe Evening News May 21, 2010: "Public Notice General Fund Budget Hearing"

Bedford Now April 17, 2010: "Township okays 2 new cell towers"

Toledo Blade April 14, 2010 : "Bedford Township tightens regulations on open burning"

Toledo Blade March 24, 2010: "Bedford Board Seeks Community Input for Possible Road Levy"

Toledo Blade March 24, 2010: "New Tax on Ballot to Fix, Maintain Playgrounds"

Toledo Blade March 3, 2010: "Parks Commission Seeks Property Tax"

Documents related to this article:

June 30, 2009 Park Operating Fund Financial Information from Bedford Township Revenue & Expenditure Report for the month ended June 30, 2009.

January 31, 2010 Park Operating Fund Financial Information from Bedford Township Revenue & Expenditure Report for the month ended January 31, 2010.

Toledo Blade March 2, 2010: "Monroe County Home Values Fall 14.67% In 1 Year"

Bedford Now January 23, 2010: "More Tax Revenue Expected To Be Lost In 2010".

Monroe Evening News May 23, 2009: Bedford residents to see 1% hike in summer property taxes.

Toledo Blade May 12, 2009: Store closings plague busy route to Bedford Township.

Bedford Now April 25, 2009: "3 township workers laid off to cut budget"

Toledo Blade April 15, 2009: "Economic woes hit Bedford Township"

Toledo Blade March 25, 2009: State grant sought for park.

Toledo Blade February 11, 2009: Firm hired to design addition to fire station.